融資信息

融資信息

專題

專題

鏈上生態

鏈上生態

詞條

詞條

播客

播客

活動

活動

OPRR

OPRR

SemiAnalysis解讀:Meta半年簽單超5GW,「雲業務」拋售可能押錯方向

简介

· Meta 在上半年与云服务和托管签订了超过 5GW 的合约,不包括自建数据中心的同步加速。

· 新增算力将用于 MSL 训练、广告推荐、Claude 私有实例和短期高价外部交易。

· CoreWeave、Nebius 的 RPO 可能会受益,但 MSL 追赶和合约灵活性仍存在风险。

Meta 引发的 Neocloud 抛售可能指向错误的方向。SemiAnalysis 在7月2日发布的报告中表示,Meta 在2026年上半年已经与云服务和托管领域签署了超过5GW的 IT 容量合约,而这个数字还不包括同步加速的自建数据中心。

这一结果与市场过去几天的担忧背道而驰。据彭博于7月1日报道,Meta 正在推动出售其超额的 AI 算力云业务,相关计划仍在进行中,策略可能发生变化。在这一消息发布后,CoreWeave、Nebius 等 Neocloud 公司的股价受到抛售的打击,投资者担心 Meta 从大客户转变为潜在竞争对手,AI 数据中心供应可能很快过剩。

SemiAnalysis 提出了另一种解释:Meta 并未减少外部采购,而是正在通过第三方 Neocloud 更快地获取容量。自2024年初以来,Meta 累计签署了近10GW的合同,目前大部分新增容量仍然通过第三方获得。对于像 CoreWeave、Nebius 这样的供应商,Meta 的订单可能继续推高其剩余履约义务(RPO)。

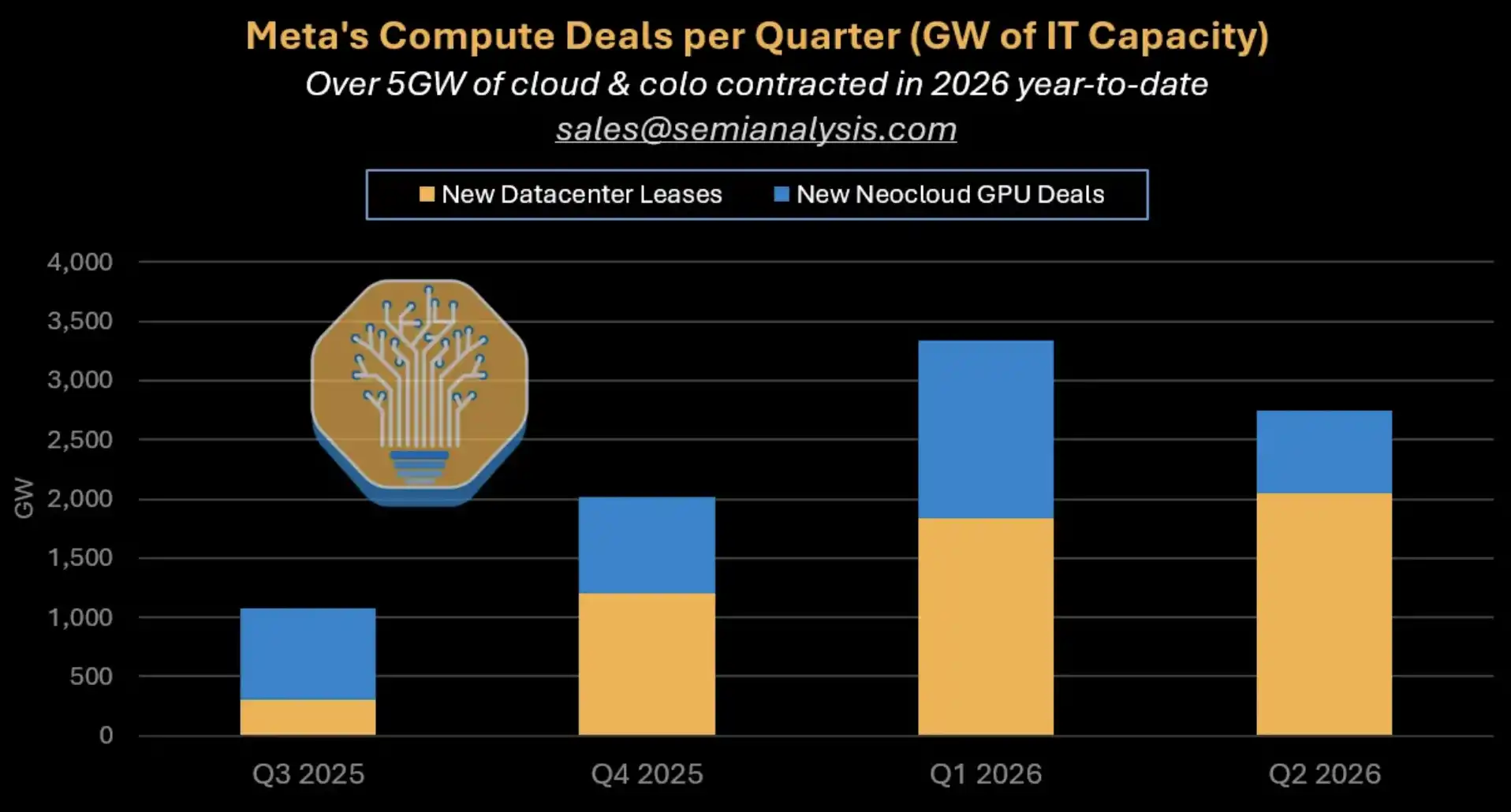

Meta 季度算力交易细分:2026年上半年云服务和托管合同累计超过5GW,区分新数据中心租赁和 Neocloud GPU 交易。

市场担心 Meta 变卖方,但报告看到的是更大的买家

这场争议的焦点并非在于 Meta 是否涉足云算力转售业务,而在于新增的大量算力到底是由谁建设、谁消化、谁承担收入风险。

如果 Meta 只是将 GPU 转租出去,转变成一家毛利率约30%的裸金属 IaaS 供应商,市场对 Neocloud 估值的担忧就显而易见。大客户廉价供应可能削弱原有供应商的议价能力,整个行业也可能陷入价格竞争之中。

但在 SemiAnalysis 的框架裡,Meta 新增容量更像一套「可選算力池」。它可以在內部前沿模型、廣告推薦、企業級模型服務和短期高價外部交易之間調配,而不是只能低價轉租 GPU。

這也是報告反駁「美國僅 5GW 數據中心在建」說法的關鍵。僅 Meta 兩大最大在建園區,合計就對應約 2.5GW 在建容量。再疊加第三方雲和托管合同,實際建設強度高於部分悲觀口徑。

換成更直接的問題,市場現在要判斷的不是 Meta 買不買算力,而是這麼多容量能不能被高價值場景吸收。

四條路消化新增算力,MSL 不是唯一出口

Meta 新增算力的第一優先級仍是 Meta Superintelligence Labs,簡稱 MSL,用於前沿模型訓練。這是資本支出最直接的敘事:Meta 要追趕 OpenAI 和 Anthropic,需要足夠大的訓練集群、人才和試錯空間。

但即使 MSL 進展不完全符合預期,Meta 也並非只能把 GPU 低價出租。

第二條路是廣告推薦系統。Meta 官方財報顯示,2026 年一季度廣告展示量同比增長 19%,平均單價同比增長 12%。Meta Engineering 此前介紹,GEM 相關訓練棧有效訓練 FLOPs 提升 23 倍,MFU 提升約 1.43 倍,GPU 規模擴大 16 倍;GEM 訓練 GPU 翻倍後,Instagram 和 Facebook Feed 廣告轉化率分別提升 5% 和 3%。

這條路對投資者更容易理解:如果更多算力能提高廣告轉化率,它就不是單純「燒錢買 GPU」,而是廣告收入和定價能力的一部分。至於報告中提到的部分排序指標提升幅度,公開獨立口徑有限,更適合作為 SemiAnalysis 模型假設,而不是已經被 Meta 官方完整確認的事實。

第三條路是模型服務平台,類似 AWS Bedrock 或 Google Vertex。SemiAnalysis 謂,Meta 正與 Anthropic 進行 Claude 私有實例相關談判,並試圖打造「代幣即服務」平台。這類容量既可用於內部,也可面向 SaaS 銷售和外部分發,但相關交易仍需用「可能落地」來看,不能當作已兌現收入。

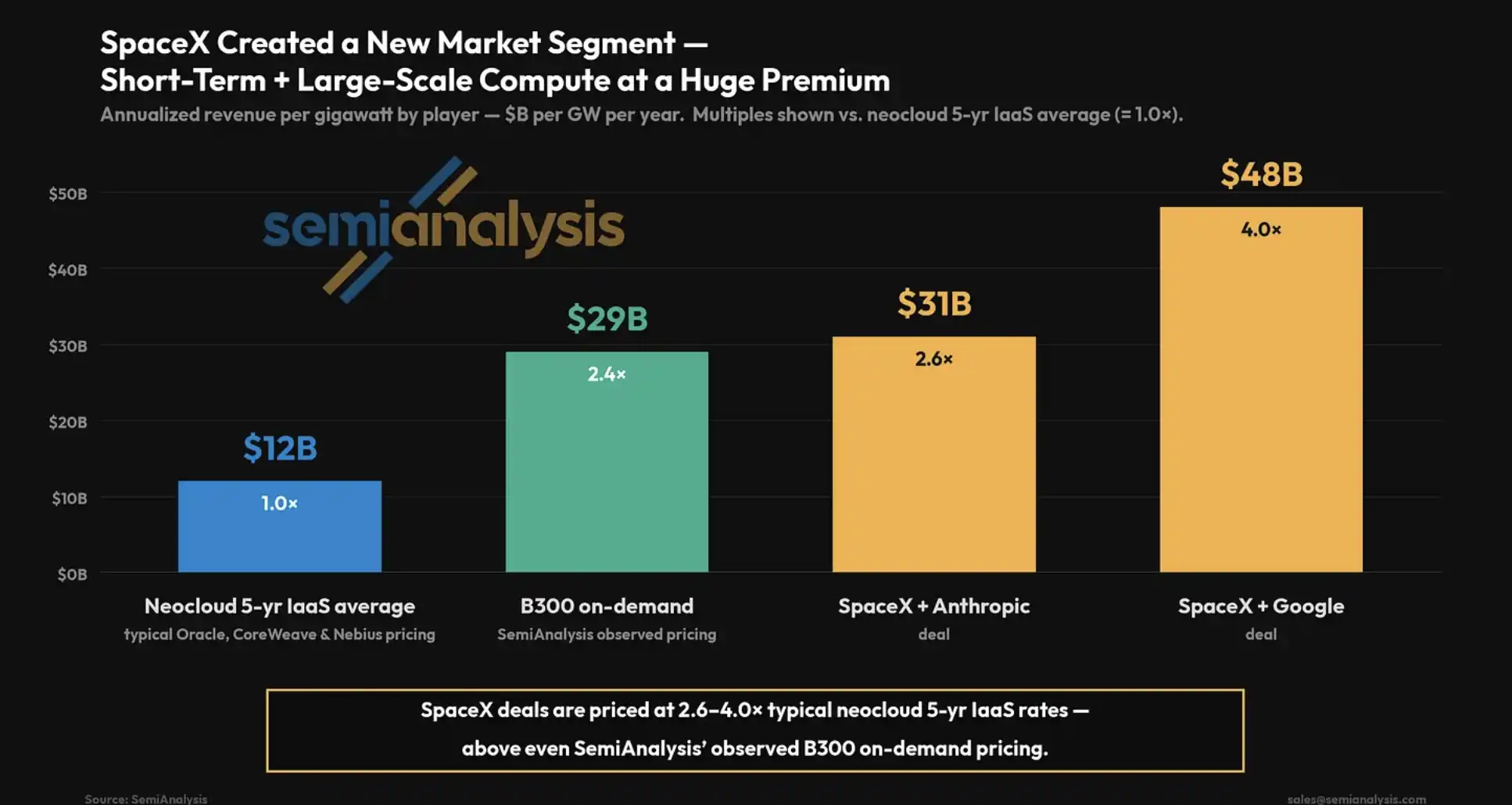

The fourth path is a large-scale, short-term, high-premium on-demand compute power trading similar to SpaceX. This is also the most impactful set of numbers in the report.

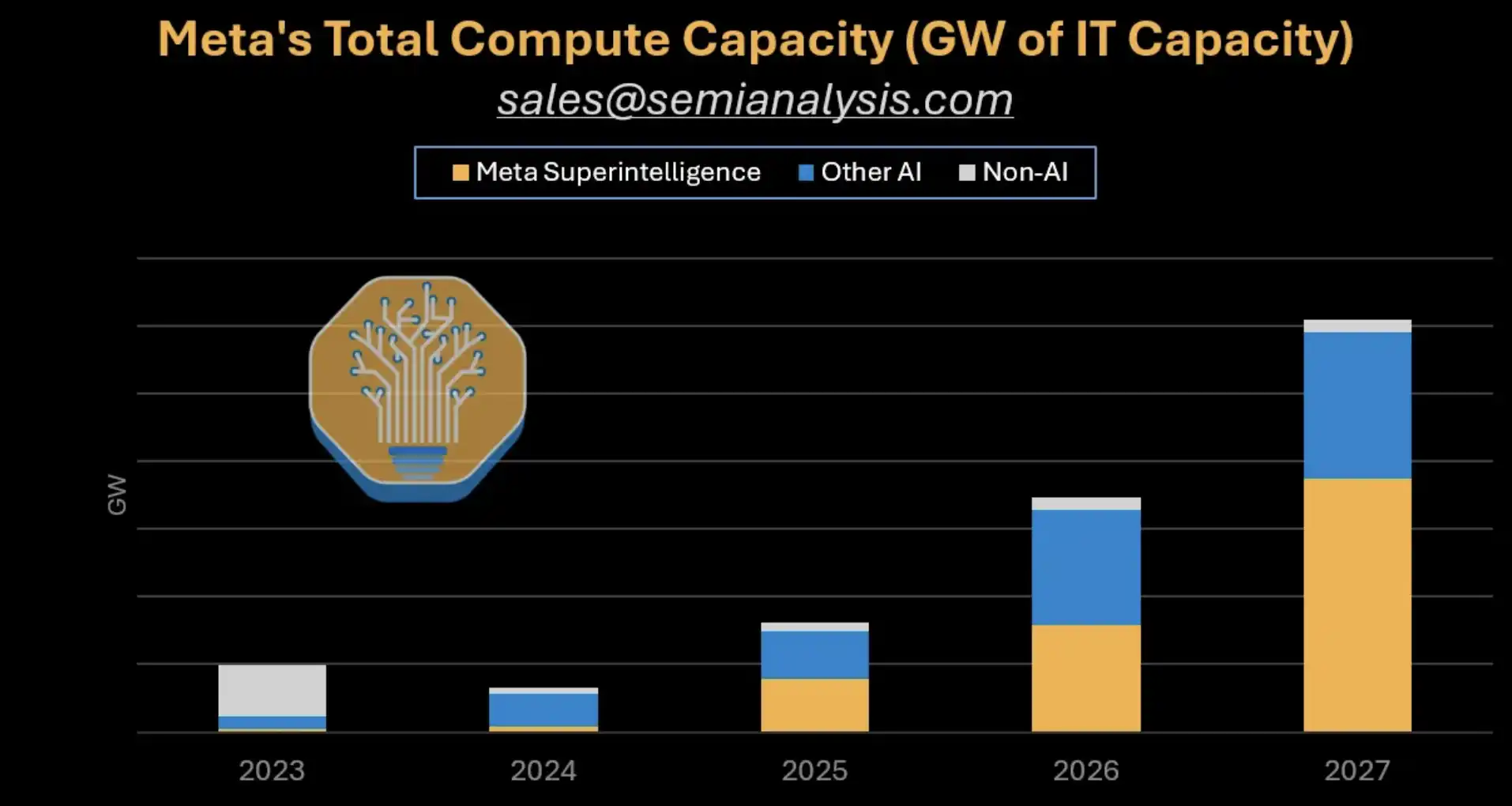

Meta's total compute capacity forecast: A stacked bar chart distinguishes MSL, Other AI, and Non-AI from 2023 to 2027, with a significant capacity expansion from 2026 to 2027.

High-Premium Short-Term Trades Transform the Revenue Imagination of "Selling Compute Power"

The key to SpaceX-style trading is not just "renting GPUs," but rather the different pricing and contract structure.

According to SemiAnalysis, the annualized revenue per GW of compute power traded between SpaceX and Anthropic is approximately $3.1 billion, which is 2.6 times the average price of a five-year IaaS contract with Neocloud. Trading with Google commands an even higher price at around $4.8 billion/GW/year, equivalent to 4 times the average. Independent public sources have provided limited confirmation of the details of these contracts. These numbers are more suited for the report's scenario, illustrating that short-term scarce compute power may command a high premium.

If Meta were to allocate only 200MW for similar external trades, based on the calculations on a publicly available page in the report, the annualized revenue could exceed $10 billion. This scale is sufficient to challenge the market's intuition about "Meta's external compute power sales": it may not necessarily be low-margin subleasing but could also involve selling time windows of quickly onboarded data center capacity to top clients in urgent need of compute power.

The report also mentions that Meta's rapidly onboarded data center design is suitable for such trades. Its value lies not in the lowest cost long-term rental but in the ability to deliver compute power more quickly when modeling companies, AI applications, or large clients temporarily require substantial compute power.

However, this remains an optional path and not a guaranteed revenue stream. Meta's ability to replicate a portion of the high-premium trading structure does not mean it has already transformed into a SpaceX-style compute power seller.

SpaceX Pricing Premium Comparison: Typical Neocloud five-year IaaS priced at around $1.2 billion/GW/year, SpaceX to Anthropic at approximately $3.1 billion, SpaceX to Google at around $4.8 billion.

The Pressure on CoreWeave and Nebius May Not Stem from Disappearing Demand

對 CoreWeave、Nebius 等 Neocloud 公司來說,市場此前的擔憂是:如果 Meta 自建或轉售算力,原本的外部採購會減少,行業訂單可能被搶走。

但從現有合同看,Meta 仍在加速使用第三方 Neocloud。公開資料顯示,CoreWeave 與 Meta 有 210 億美元合同,Nebius 與 Meta 的合同最高可達 270 億美元。Nebius 在 2026 年一季度股東信中稱,其簽下第二個 Meta 大單,合同容量超過 3.5GW,並提到 Microsoft、Meta 客戶承諾。

Meta 願意為速度支付溢價,也是第三方供應商仍有價值的原因。只要 Meta 認為算力可以被 MSL、廣告系統、模型服務或短期高價交易吸收,就有理由讓 Neocloud 先建集群,而不是等待自建項目慢慢交付。

「產能過剩」也不能只看總 GW 數。AI 數據中心真正緊缺的部分,往往不是紙面電力,而是可用 GPU、網絡、機房交付速度、客戶遷移成本和合約靈活性。Meta 如果需要快速拿到成片容量,第三方 Neocloud 仍然有用。

這不等於 Neocloud 公司沒有風險。它們的估值仍取決於大客戶集中度、融資成本、GPU 折舊、長期合約質量,以及客戶是否真的把未來容量吃下去。Meta 帶來的 RPO 增長,如果對應的是高資本開支和高客戶集中度,市場仍會打折。

MSL 追不上,5GW 就會變成資本開支壓力

這份報告最需要克制的地方,是不能把 Meta 的每條可選路徑都寫成已經成功。

MSL 能否追上 OpenAI 和 Anthropic 仍有很大不確定性。前沿模型競爭不是單靠 GPU 數量就能解決,數據策略、研究團隊、訓練穩定性、產品分發和推理成本都會影響結果。

合約條款也會影響風險大小。SemiAnalysis 稱,類似 SpaceX 的交易通常包含 90 天雙向取消條款。這種安排給了買賣雙方靈活性:如果某個團隊進展不佳,算力可以快速回收;如果需求變化,也不至於被長期鎖死。相關條款細節缺少公開獨立確認,更適合作為報告假設處理。

對 Meta 來說,靈活性本身有價值。它可以先給 MSL 留下足夠電力和 GPU 做前沿嘗試,同時把一部分容量轉向廣告推薦、Claude 私有實例或高價短單。

反過來,如果 Meta 最終簽下大量缺少靈活退出安排的長期算力交易,風險就會上升。一旦前沿模型追趕不順,廣告和模型服務又無法消化新增容量,超過 5GW 的新外採算力會更直接變成資本支出壓力。

歡迎加入律動 BlockBeats 官方社群:

Telegram 訂閱群:https://t.me/theblockbeats

Telegram 交流群:https://t.me/BlockBeats_App

Twitter 官方帳號:https://twitter.com/BlockBeatsAsia