融資信息

融資信息

專題

專題

鏈上生態

鏈上生態

詞條

詞條

播客

播客

活動

活動

OPRR

OPRR

十年監管終於明確,加密原生邏輯的勝利

BTC、ETH、SOL、XRP、DOGE、SHIB。

These names were written together for the first time in an SEC regulatory document, with a few words added behind them: not securities.

On the evening of March 17, 2026, the SEC and CFTC jointly issued a 68-page interpretive document, formally providing a systematic qualitative analysis of the securities attributes of crypto assets. This marks the first time at the federal level in the United States that specific tokens have been formally named and classified in a regulatory interpretation. The document also replaces the SEC's previous "Investment Contract Analysis Framework" released in 2019, which was a primary reference for industry compliance assessments.

This document had a clear timeline.

In January 2025, SEC Acting Chair Mark T. Uyeda established the Crypto Task Force to clarify the application boundaries of securities laws to crypto assets. In the same year, in July, the President's Digital Asset Market Working Group issued a report recommending that the SEC and CFTC use their existing powers to provide regulatory clarity to the industry.

SEC Chair Paul S. Atkins then launched Project Crypto, which was upgraded to a joint SEC-CFTC project in January 2026. During this period, the Crypto Task Force received over 300 public comments from issuers, investors, law firms, audit firms, and others.

In other words, this document represents the "unified answer" given by two federal regulatory agencies after more than a year of industry negotiations and policy coordination.

Five Lines to Draw the Whole Map

In this document, the SEC classifies crypto assets into five categories. The core criterion for judgment is the four elements of the Howey Test.

The first category is "Digital Commodities." This is the most anticipated part of the entire document, as the SEC provides a specific list of names. BTC, ETH, SOL, XRP, ADA, AVAX, DOGE, SHIB, LINK, DOT, LTC, BCH, HBAR, XLM, XTZ, APT, a total of 16 tokens are explicitly listed in the text. The footnote also mentions that Algorand (ALGO) and LBRY Credits (LBC) also fall into this category.

SEC 給出的判斷邏輯是:這些代幣的價值與其所在功能性加密系統的程式化運行內在關聯,由供需驅動,而非來自對他人管理努力的利潤期待。

第二類是「數位藏品」(Digital Collectibles)。CryptoPunks、Chromie Squiggles、WIF(dogwifhat)、VCOIN 被點名列入。Meme 幣在這裡找到了自己的位置,SEC 認為它們的價值由「藝術、娛樂、社交或文化意義」驅動,類似實體收藏品,不構成證券。

第三類是「數位工具」(Digital Tools)。ENS 域名和 CoinDesk 的 Microcosms NFT 門票被列為例子。這類資產的特徵是執行實際功能,如會員憑證、身份識別、產權憑證,很多是靈魂綁定不可轉讓的。

第四類是「穩定幣」(Stablecoins)。根據已經通過的《GENIUS 法案》,合規發行商發行的「支付型穩定幣」被法律明確排除在證券定義之外。但 SEC 同時保留了對不符合該法案標準的穩定幣的管轄權。

第五類是「數位證券」(Digital Securities)。這是唯一被明確確認為證券的類別。但 SEC 沒有在文件中點名任何具体代幣屬於此類。

這五類之間的邊界並非絕對。SEC 自己也承認,存在跨類別的混合型資產,以及不屬於任何一類的加密資產。但這套分類框架的意義在於:它第一次把「什麼是證券、什麼不是」從法庭辯論拉到了監管執行層面。

四類鏈上行為,統一定性

代幣分類之外,這份文件的另一個重大貢獻是對挖礦、質押、打包、空投四類核心鏈上行為做出了統一定性。

協議挖礦(Protocol Mining)不構成證券發售。無論是單人挖礦還是加入礦池,挖礦行為本身是網絡維護活動,新產出的代幣是協議層面的程式化獎勵,不涉及投資合同關係。

協議質押(Protocol Staking)不構成證券發售。這個判斷覆蓋了四種場景,單人質押、委托給第三方但自己保管密鑰、委托給托管方質押,以及流動性質押。SEC 在文件中明確,質押收益來自協議預設的程式化分配,而非某個管理團隊的經營努力。對於流動性質押產生的 LST(如 stETH),SEC 認定它們僅是底層質押資產的「收據」,不屬於衍生品,也不構成證券。

資產打包(Wrapping)不構成證券發售。將 BTC 打包成 WBTC 在以太坊上使用,只是一個技術層面的互操作性操作,不改變底層資產的性質。

空投(Airdrops)不構成證券發售。只要接收者沒有提供資金、商品或服務作為對價,免費的代幣分發不滿足 Howey 測試中「投入資金」的要件。

這些判斷對行業的直接影響是,DeFi 協議的核心機制,staking、wrapping、airdrop,全部被從證券法的射程範圍內移出。過去三年裡,每一個運營質押服務或發放空投的專案方都在擔心的問題,現在有了一個來自聯邦監管機構的統一回答。

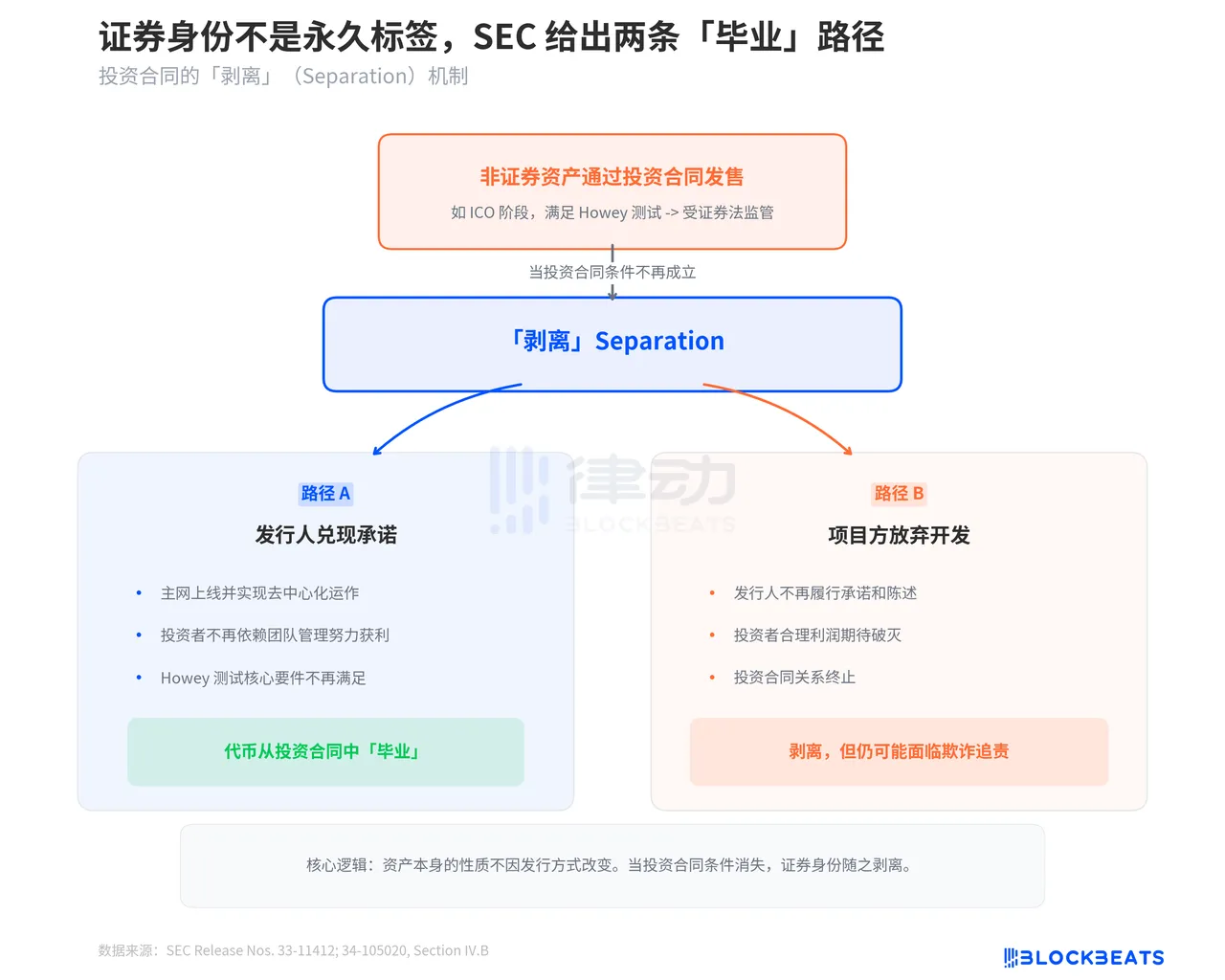

證券身份不是永久標籤

這份文件中最值得細讀的部分,可能是 SEC 對「剝離」(Separation)機制的闡述。文件明確規定,一個本身不是證券的加密資產,可以因為發行方式(如通過投資合同發售)而被納入證券監管。但當投資合同的條件不再成立時,這個資產可以與證券身份「剝離」。

SEC 給出了兩種剝離情形。第一種是發行人兌現了承諾。比如一個專案在 ICO 時承諾將開發去中心化網絡,當網絡真正上線並實現去中心化運作後,投資者不再需要依賴發行團隊的管理努力來獲利,Howey 測試的核心要件不再滿足,代幣就從投資合同中「畢業」了。

第二種情形更有意思,就是專案方「放棄了」。如果發行人不再履行其在投資合同中做出的承諾和陳述,投資者對「他人努力帶來利潤」的合理期待也隨之破滅,投資合同關係同樣終止。但 SEC 強調,這不意味著發行人可以逃脫責任,他們仍可能面臨欺詐追責。

這個「剝離」機制的真正意義在於,它為加密專案提供了一條合規路徑。從 ICO 到主網上線到充分去中心化,不再是法律灰色地帶的冒險,而是一條有明確終點的監管隧道。走完了,就出來了。

68 頁。九個章節。18 個被點名的代幣,6 種被定性的鏈上行為,2 條「畢業」路徑。SEC 用了一年多的時間收集了 300 多份意見書,最終跟 CFTC 聯手交出了這份答卷。它不完美,穩定幣的邊界仍有模糊地帶,「數字證券」類別下沒有給出任何具體例子,混合型資產的判斷標準也留了餘地。

但對一個過去被批評為「靠執法代替監管」的機構來說,這份文件至少做到了一件事情:把規則寫在了紙上,而不是寫在訴狀裡。

歡迎加入律動 BlockBeats 官方社群:

Telegram 訂閱群:https://t.me/theblockbeats

Telegram 交流群:https://t.me/BlockBeats_App

Twitter 官方帳號:https://twitter.com/BlockBeatsAsia